do pastors pay taxes on their income

Churches that do not do their homework on pastoral compensation tend to underpay their pastors. According to the Bureau of Labor Statistics in 2016 the average salary was 45740 annually or 2199 hourly.

Pin On Products

Generally retired ministers do not pay SECA tax on their retirement income.

. Eligible distributions before retirement taken as a housing allowance may be subject to SECA tax. Regardless of whether youre a minister performing ministerial services as an employee or a self-employed person all of your earnings including wages offerings and fees you receive for performing marriages baptisms funerals etc are subject to income tax. At the low end members of the clergy earned only 23830 annually and the highest earning pastors earned 79110.

Therefore the minister will have to pay tax to the IRS in quarterly installments throughout the year. From a personal income perspective the first thing to understand is that the income tax code takes the position that any money paid to or for an employee is income unless specifically excluded by the tax code. According to IRS requirements a pastor employed by a congregation must file income taxes the same as any other employee of a business or organization.

The minister however must pay the Medicare and Social Security taxes herself in a self-employment quarterly tax payment or by asking their employer to withhold part of their income with an IRS W-4 form. For specific rules see. This means a church normally wont withhold income tax and never should withhold Social Security tax for clergy.

Many pastors request no raises but would still appreciate one. He can request that the church withhold 800 of income tax from each months paycheck. They can exempt a housing allowance or the value of residence in a parsonage.

Pastors in the United States pay federal income taxes on their salaries and they pay FICA they may or may not be considered self-employed. Even though the minister can only elect withholding of income taxes he can use these tax payments against both income and self-employment tax since they are added together on his personal income tax return Form 1040. If excess housing allowance is taken it must be allocated as income.

Honoraria and fees that you receive from individuals for marriages baptisms funerals masses etc are usually considered income. Clergy can request that an additional amount of income. Note however that even though clergy pay SECA tax most ministers are considered employees and should receive a Federal Form W-2 from their employer.

Do pastors pay federal taxes. Generally there are no income or Social Security and Medicare taxes withheld on this income. So in a way they have income that the rest of us would have to pay taxes on.

Members of the clergy ministers members of a religious order and Christian Science practitioners and readers and religious workers church employees must pay self-employment tax SE tax. The IRS considers any money pastors directly receive from. If you receive as part of your salary for services as a minister an amount officially designated in advance of payment as a housing allowance and the amount.

The housing allowance will allow you to reduce your federal taxes by the amount of your allowance and thus reduce your federal taxable income. Still ministers have tried to argue against this ruling for decades. What constitutes retirement for purposes of these rules about SECA tax and the housing.

A ministers housing allowance sometimes called a parsonage allowance or a rental allowance is excludable from gross income for income tax purposes but not for self-employment tax purposes. Priests and Pastors pay income taxes on their salaries but are exempt from taxes on their parsonage allowance if it meets certain requirements. Pastors are able to reduce their.

105 the United States Supreme Court has ruled that the First Amendment guaranty of religious freedom is not violated by subjecting ministers to the federal income tax. But for a pastor there are two sides to taxesthe federal and the SECA. But clergy are both exempt from federal income tax withholding and considered self-employed for Social Security tax purposes.

The Clergy Housing Allowance Exemption Reduces a Pastors Taxable Income. It can be confusing especially for those who are new pastors or those who are new to this allowance. This is the median.

If you are a member of the clergy you should receive a Form W-2 Wage and Tax Statement from your employer reporting your salary and any housing allowance. According to the IRS a pastor is an employee who performs services for a church or organization that has legal control over how they carry out those services. And as a rule of thumb you could seek to estimate what the mean income is for families in the church and use that as a basis for compensation for the pastor.

However retired ministers may not have to pay SECA taxes on their income designated as housing allowance. Since 1943 Murdock v. Pastors fall under the clergy rules.

A pastors housing allowance is subject to SSFICA tax but not income tax. Answer 1 of 8. Otherwise pastors are required make quarterly payments like self-employed people do.

In addition to a pastors base salary there are some items the church may provide as fringe benefits to the pastor or other. Ministers are not exempt from paying federal income taxes. Pastors may voluntarily choose to ask their church to withhold their taxes by completing a W-4 form requesting that a certain amount be withheld.

When a minister works for a church the church can withhold income tax. Many pastors opt to be designated a church employee as opposed to maintaining self-employment status solely for retirement benefit purposes. If a pastor earns a salary the IRS considers them to be a common-law employee and their wages are taxable for withholding purposes.

The following income is included in the SE tax calculation on Schedule SE. Clergy must pay quarterly estimated taxes or request that their employer voluntarily withhold income taxes. Salaries and fees for your ministerial services.

Money received from weddings offerings special events outside their church would be reported on Schedule C for self. A pastor may be unclear about their personal tax bracket due to additional taxable income from relocation housing and services such as performing marriages baptisms and funerals. Generally a minister must pay self-employment taxes on the wages earned their.

The salary from the W2 is reported on the form 1040. Most pastors are paid an annual salary by their church. They are considered a common law employee of the church so although they do receive a W2 their income is reported in different ways.

Pin On Starting And Promoting Your Own Business

What Taxes Can Churches Withhold For Pastors The Pastor S Wallet

Pastor Taxes Pastor Income Tax Rules Aplos Academy

Calculator With Text On Screen Tax Concept Stock Photo Aff Screen Text Calculator Tax Ad Deduction Tax Tax Forms

Irs How To Handle Senior Pastor Tax Return Seniorcare2share

2022 Church Clergy Tax Guide Clergy Financial Resources

How Pastors Pay Federal Taxes The Pastor S Wallet

Tax Preparation For Pastors And Clergy Tax Preparation Our Services

Who Is Responsible For The Clergy Housing Allowance The Pastor Or The Church The Pastor S Wallet

How To Handle Clergy Tax

How The Clergy Cash Or Rental Housing Allowance Works The Pastor S Wallet Housing Allowance Finance Investing Clergy

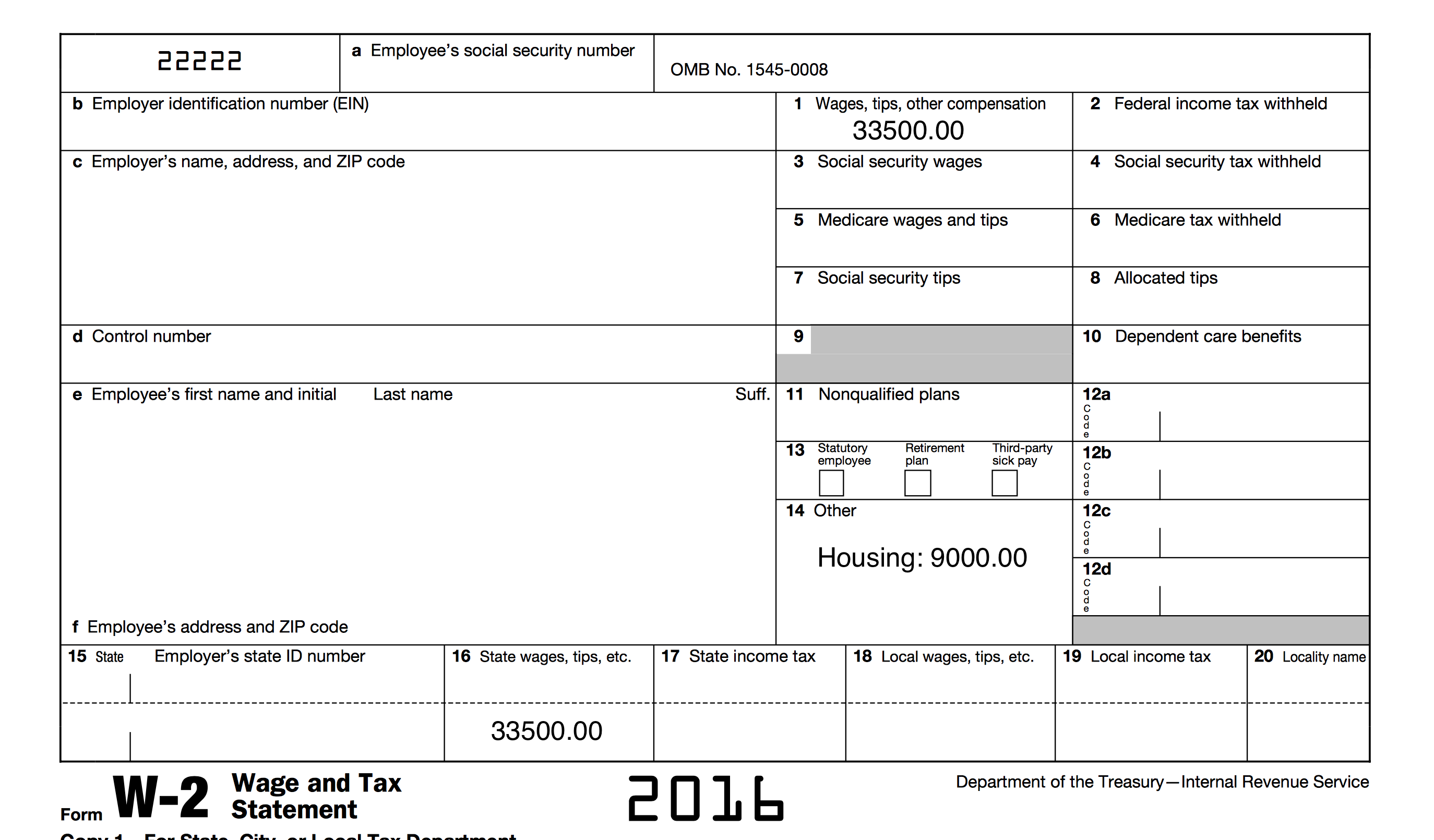

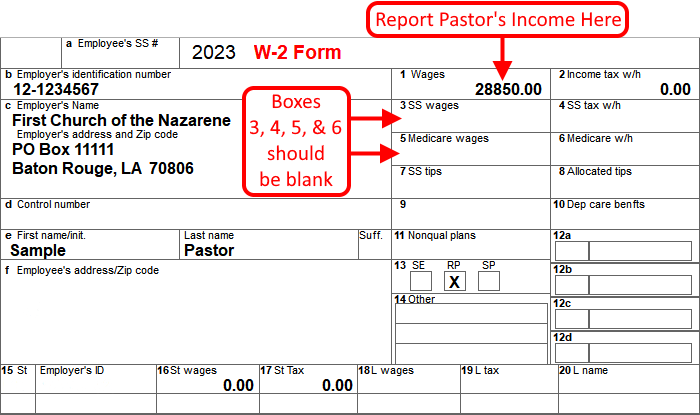

Example Of Pastors W 2 Form

Church Tax Conference For Small Churches Alabama Baptist State Board Of Missions

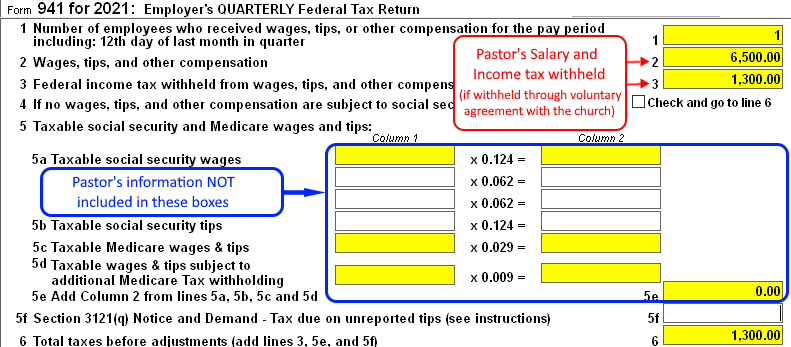

Nts Faq Reporting Pastor S Income On Forms W 2 And 941

Nts Faq Reporting Pastor S Income On Forms W 2 And 941

Clergy Taxes

How To Make Quarterly Estimated Tax Payments For Ministers The Pastor S Wallet

Calling All Churches And Non Profit Organization Let S Talk About Building Kingdom Wealth Join Us Tonight 8pm Es The Kingdom Of God Empowerment Text Me

Pin On Girl Boss Tips Tricks For Saving On The Job